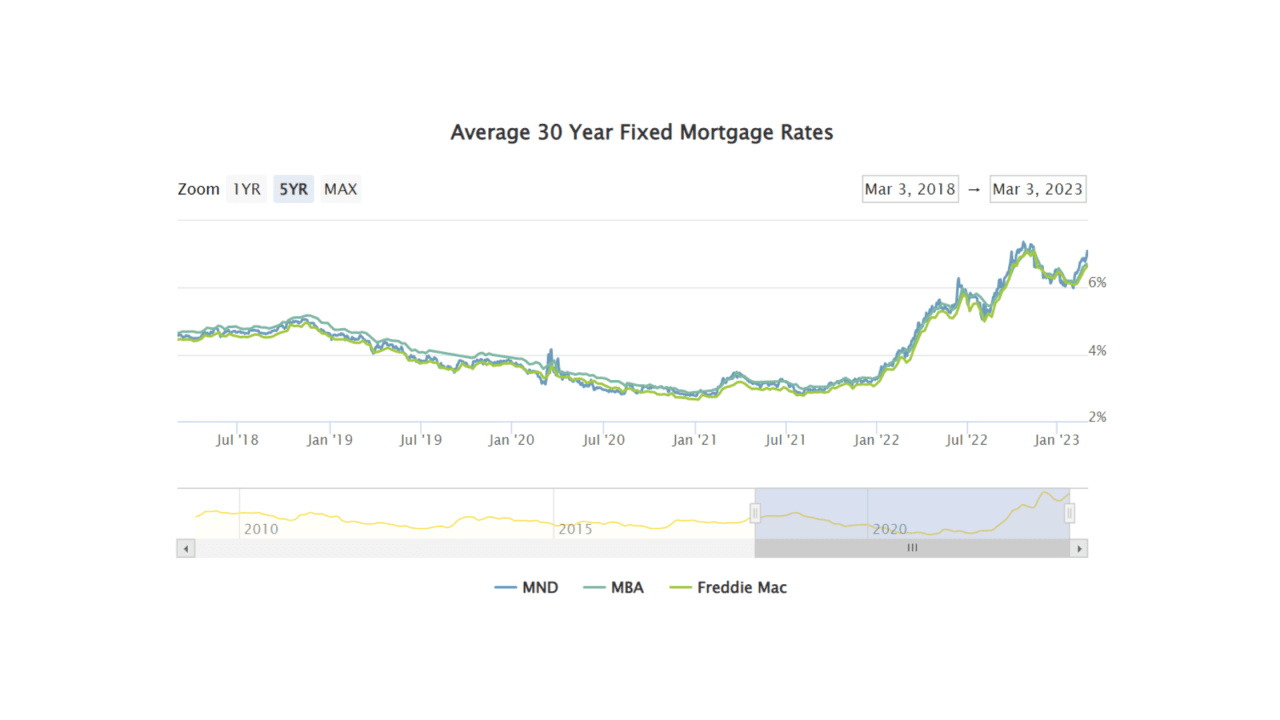

Mortgage rates have been on the rise due to several factors. While the bond market is typically responsible for movement in interest rates, recent economic data (a strong job market and low unemployment rate) has caused traders to worry about inflation and economic growth, leading to higher interest rates

Additionally, changes in upfront fees required for all conforming mortgages by the regulator overseeing Fannie and Freddie have led to a potential increase of 0.125% in rates for borrowers. These factors have contributed to the average lender's 30-year fixed rate rising to the low 7's for a well-qualified scenario. However, our local lenders at PNC Bank are still quoting interest rates below 7%. Current rates are shown below.

The Fed will announce their target for short-term interest rates again on March 22, it’s expected that mortgage interest rates will increase as a result of this meeting’s outcomes. More on that later this month.

Current Interest Rates:

From the desk of Khue Dang at PNC Bank:

Jumbo Loans

(Assumptions: Purchase, Loan Amount $726,201+, 20% down payment, 740+ credit score, 30 day rate lock period)

30 Year Fixed- 6.375%- APR 6.391%

10/1 ARM- 6.25%- APR 6.970%

Conventional Loans

(Assumptions: Purchase, Loan Amount $726,200 and lower, 20% down payment, 740+ credit score, 30 day rate lock period)

30 Year Fixed- 6.75%- APR 6.818%

20 Year Fixed- 6.625%- APR- 6.713%

15 Year Fixed- 6.0% APR 6.103%

Mortgage Fact: Who's Fannie and Freddie?

I used the terms "Fannie and Freddie" earlier. For those who aren't sure what this means, here's a brief explanation - they're colloquial terms used to refer to two US government-sponsored enterprises (GSEs) - Fannie Mae (the Federal National Mortgage Association) and Freddie Mac (the Federal Home Loan Mortgage Corporation).

Both entities were created by Congress to provide liquidity to the mortgage market by purchasing mortgages from lenders, pooling them, and selling them as mortgage-backed securities to investors. This helps to keep interest rates low and allows more people to afford homeownership. Both entities were privatized in the late 1960s and early 1970s, but the government continues to play a significant role in their operations. In 2008, both companies were placed under conservatorship by the government in response to the housing market collapse and financial crisis.

Have the best weekend!

Yours in rates and real estate,

Alex